You've been working with your financial advisor for years. The relationship is solid. They're competent, responsive, and you trust them.

And they charge 1% of your assets under management annually.

That probably sounded reasonable when you started. It might still sound reasonable now. A percentage point doesn't feel like much. There’s a question though worth asking as your portfolio has grown over the years…

Is that 1% fee still fair?

Not whether your advisor is worth working with. Not whether financial advice has value. It's whether the fee structure itself makes sense for someone with substantial assets who's already done the heavy lifting of building wealth.

Shall we look at the numbers?

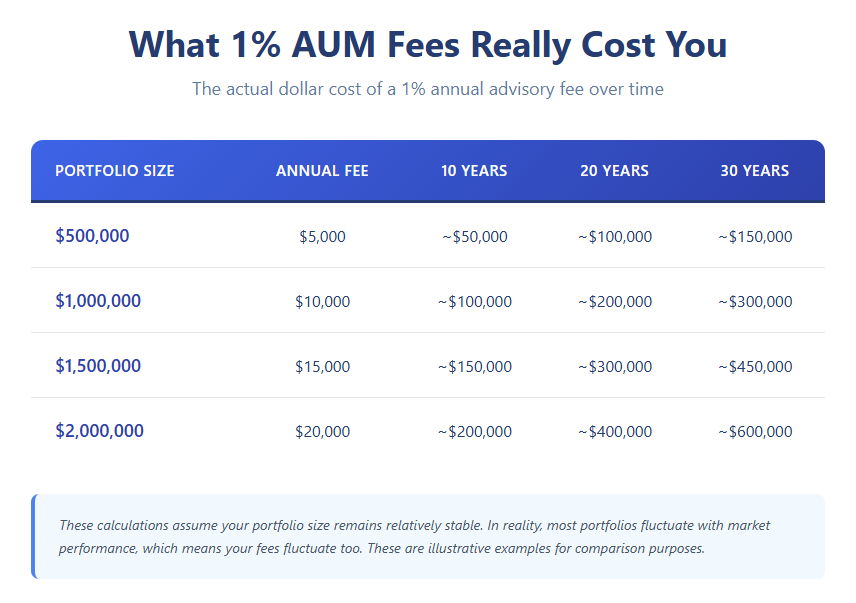

What 1% Really Costs You

Numbers make this clearer than any argument I could make. Here's what a 1% AUM fee actually costs in real dollars over time.

Let's look at what happens when your portfolio appreciates.

The Growth Scenario:

You start retirement with $1.5 million. You're paying $15,000 per year (1% AUM fee).

After several good market years, your portfolio grows to $2 million. You didn't contribute a dollar. The market appreciated.

Your annual fee just increased from $15,000 to $20,000.

Over the next 20 years, that $5,000 annual difference adds up to roughly an additional $100,000 in fees, assuming relatively stable portfolio values. You did the saving decades ago. The market did the appreciating. But the fee grew alongside your assets.

Now, in all likelihood there is a tier structure to the percentage you pay as your assets grow but the point remains.

According to research from the CFP Board, the median fee for assets under management hovers around 1% for portfolios in this range, though fees can vary from 0.5% to 2% depending on firm size and services offered.

The Original Logic Behind AUM Fees

To be fair, the assets under management fee structure wasn't created with malicious intent.

The logic goes like this. Tying advisor compensation to portfolio size aligns incentives. If your portfolio grows, your advisor benefits. If your portfolio shrinks, your advisor feels the pain too. It's a partnership.

For smaller portfolios, this model can make sense. Someone with $200,000 saved might struggle to pay a meaningful flat fee for planning services. A percentage-based fee makes professional advice accessible.

The AUM model also simplified billing in an era before easy online payments and automated systems. One annual percentage calculation. Clean. Simple. Everyone understood it.

And honestly, for advisors building a practice, AUM fees provided recurring revenue that made business planning possible. That's not inherently wrong.

But as portfolios grow into seven figures and beyond, the math starts telling a different story.

Questions About Fee Structures and Portfolio Growth

As portfolios grow into seven figures and beyond, it's worth considering whether your fee structure still aligns with the service provided.

For many clients, the work required to manage a $1.5 million portfolio may not be dramatically different from managing a $750,000 portfolio. Annual reviews, rebalancing, tax planning, withdrawal strategies, and Social Security optimization often look similar regardless of portfolio size.

Some advisors would argue that larger portfolios carry more fiduciary responsibility and require more sophisticated strategies. That's a fair point. Others would say the core work remains comparable even as assets grow.

This raises a reasonable question. If your portfolio doubled primarily due to market appreciation rather than increased service complexity, is it fair for your advisory fee to double as well?

Different advisors and clients will answer this differently. Some value the alignment of interests that percentage-based fees create. Others prefer fee transparency that isn't tied to market performance. Neither approach is inherently right or wrong, but it's worth understanding what you're paying and why.

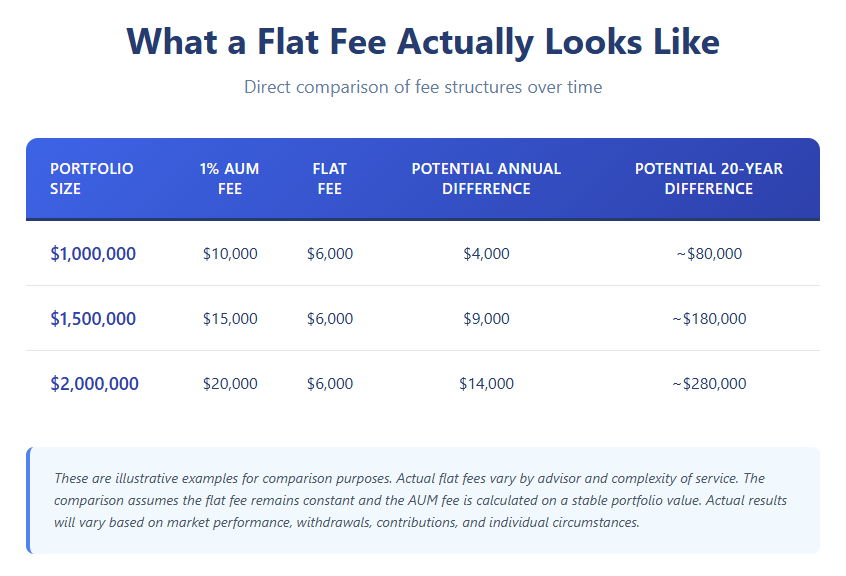

What a Flat Fee Actually Looks Like

A flat fee structure takes a different approach.

Instead of paying a percentage of assets, you pay a fixed annual fee for comprehensive financial planning and advice. The fee is based on the complexity of your situation, the scope of services you need, and the time required to serve you well, not the size of your portfolio.

Now here's where it gets more interesting. What happens when your portfolio grows?

If your $1.5M portfolio grows to $2M:

- AUM client fee increases from $15,000 to $20,000 (33% fee increase)

- Flat fee client fee typically stays at $6,000 (no automatic increase tied to portfolio growth)

- Potential annual difference: $14,000

- Potential 20-year difference: ~$280,000

These examples illustrate how different fee structures respond to portfolio growth. Actual results will vary based on market performance, withdrawals, contributions, and individual circumstances.

For many clients, the work required from their advisor doesn't change significantly when their portfolio grows from market appreciation. The relationship looks similar. The meetings look similar. The advice may look similar. But under an AUM model, the fee increases automatically.

A flat fee structure provides clarity. You know exactly what you're paying each year. There's no calculation required. The fee is the fee, and it's based on the service you're receiving rather than your account balance.

Considerations Around Fee Structures

Different fee structures can create different dynamics in the advisor-client relationship. It's worth understanding these as you evaluate what makes sense for your situation.

Potential considerations with AUM fee structures:

The Roth conversion question. Should you convert $100,000 from your traditional IRA to a Roth IRA? It might make sense from a tax planning perspective. But if your advisor charges AUM fees and your Roth IRA isn't under their management, they're recommending a strategy that reduces their revenue. Most advisors navigate this with integrity, but the structure creates a dynamic worth being aware of.

The pay off the mortgage question. Should you use $300,000 from your brokerage account to eliminate your mortgage? That might be the right move for peace of mind and cash flow. But your AUM advisor would see fees reduced on $300,000 of managed assets. Again, good advisors put clients first, but the fee structure creates tension.

The asset location question. Where you hold different assets (taxable vs retirement accounts, under management vs outside management) can create revenue implications for AUM advisors that may not align with your optimal tax strategy.

Potential considerations with flat fee structures:

The growth incentive question. If an advisor's fee doesn't increase when your portfolio grows, do they have less incentive to help maximize your returns? Some would argue the fiduciary duty and professional reputation provide sufficient motivation. Others prefer the direct alignment of AUM fees.

The time allocation question. Flat fee advisors might have an incentive to minimize time spent per client since their revenue is fixed regardless of hours invested. AUM advisors, conversely, might have incentive to spend more time since their revenue is tied to keeping and growing client assets.

The complexity mismatch question. If your situation becomes significantly more complex over time but your flat fee doesn't adjust, the advisor might not be fairly compensated for increased work. Conversely, if your situation simplifies, you might overpay relative to service needed.

Both fee structures have trade-offs. The key is understanding them and choosing what aligns with your priorities and comfort level.

Is AUM Ever the Right Choice?

Yes, in many situations.

If you're early in your wealth-building journey with a smaller portfolio, AUM fees can make financial advice accessible. Paying $2,000 annually (1% of a $200,000 portfolio) might be more manageable than a $6,000 flat fee when you're still building toward retirement.

If you value having your advisor's compensation directly tied to your portfolio performance, AUM fees create that alignment. Some clients find this comforting and prefer this structure for that reason.

If your financial situation is genuinely complex with multiple businesses, real estate holdings, trust structures, and estate planning needs, percentage-based fees might align well with the significant ongoing work required. Though even then, a flat retainer based on complexity rather than a percentage of assets is worth considering.

If you're receiving active portfolio management with truly customized investment strategies rather than allocation to index funds or model portfolios, there may be merit to performance-linked compensation structures.

The key question is whether the fee structure matches the value delivered and the work required for your specific situation.

Questions to Ask Your Current Advisor

If you're currently paying AUM fees and wondering whether it makes sense to continue, here are questions worth raising.

What exactly am I paying for each year? Get specific. Annual planning meetings? Ongoing portfolio monitoring? Tax planning? Estate planning coordination? Understand the full scope of service.

How has my fee changed as my portfolio has grown? Look at the actual dollar amounts over the past five or ten years. The percentage might have stayed the same, but the dollars have likely grown significantly if your portfolio appreciated.

How does my fee adjust if my portfolio declines? In theory it decreases proportionally, but it's worth understanding how that actually works in practice, including any minimum fees.

Do you offer alternative fee arrangements? Some AUM advisors offer flat fee or retainer structures for certain clients. If you don't ask, you won't know.

How would an alternative fee structure compare to my current arrangement? If they offer multiple models, ask for a direct comparison based on your specific situation.

These aren't confrontational questions. They're reasonable inquiries about a significant ongoing expense. A good advisor should be comfortable discussing fee structures transparently.

The Fee Conversation Nobody Wants to Have

Here's what makes this topic uncomfortable.

If you've worked with your advisor for years, there's likely genuine relationship equity built up. They've helped you through market downturns, life transitions, and difficult decisions. That has real value.

Raising questions about fees can feel like you're devaluing the relationship or suggesting they're overcharging you. That's not necessarily the case. You can simultaneously value the advice you've received and recognize that the fee structure might not be optimal for your current situation.

Think of it this way. Your advisor built their practice around a certain business model. That's fine. You built your wealth through decades of disciplined saving and smart decisions. That's also fine. The question is whether the current arrangement still serves both parties fairly as your circumstances have evolved.

Most advisors worth working with will have an honest conversation about fees if you initiate it. If an advisor gets defensive or dismissive when you ask reasonable questions about a significant ongoing expense, that response itself might be telling you something important about the relationship.

What This Means for Your Wealth

Let's bring this back to your specific situation.

If you have $1 million or more saved for retirement, you're in the top 10% of American households according to the Federal Reserve's Survey of Consumer Finances. You've done the hard work. You've built real wealth.

The potential difference between paying 1% AUM fees and a $6,000 annual flat fee could range from $4,000 to $14,000 annually, depending on your portfolio size. Over a 20-30 year retirement, that potential difference could reach $80,000 to $400,000 or more, though actual results will vary based on many factors including market performance, withdrawals, and fee adjustments over time.

That's a substantial amount. That's years of healthcare costs in late retirement. That's financial security for your spouse. That's gifts to grandchildren or donations to causes you care about.

The question isn't whether financial advice has value. It does. The question is whether you're paying a fair price for the specific advice and service you're receiving.

Frequently Asked Questions

What is the average fee for a financial advisor?

According to industry research from NAPFA and other sources, AUM fees typically range from 0.5% to 2%, with 1% being common for portfolios in the $500,000 to $2 million range. Flat fee arrangements for comprehensive planning typically range from $3,000 to $20,000 annually depending on complexity. Hourly rates range from $200 to $400 per hour for project-based work.

Is 1.5% too high for a financial advisor?

For most clients with substantial assets, 1.5% is on the higher end of typical pricing. A 1.5% fee on a $1 million portfolio is $15,000 annually. On a $2 million portfolio, that's $30,000 per year. Unless you're receiving extraordinarily complex, highly customized service, that fee level may be worth evaluating compared to alternatives. Many advisors charge 0.75% to 1% for portfolios in this range, and flat fee arrangements often provide comparable service at different price points.

How much does a flat fee financial advisor cost?

Flat fee advisors typically charge between $3,000 and $20,000 annually for comprehensive financial planning, though fees vary significantly based on complexity. Some advisors charge a consistent flat fee regardless of portfolio size, since the work required may be similar whether you have $1 million or $3 million. For example, some advisors might charge $6,000 annually for comprehensive planning across a range of portfolio sizes. Unlike AUM fees, flat fees typically don't automatically increase when your portfolio grows from market appreciation.

Can I negotiate financial advisor fees?

Often, yes. Many advisors, particularly those charging AUM fees, have some flexibility on their fee schedules, especially for larger portfolios. If you have $1 million or more, it's reasonable to ask whether they offer reduced rates for larger accounts or alternative fee structures. Some advisors will negotiate, others have firm pricing. You won't know unless you ask.

What percentage should I pay a financial advisor?

There's no universal "should," but context matters. For smaller portfolios under $500,000, a 1% to 1.5% AUM fee might be reasonable if flat fee alternatives are cost-prohibitive. For portfolios between $500,000 and $1 million, consider whether fees below 1% or flat fee arrangements make more sense. For portfolios above $1 million, comparing different fee structures can help you understand what's fair for your situation.

Are financial advisor fees tax deductible?

Not for most people currently. The Tax Cuts and Jobs Act of 2017 eliminated the deduction for investment advisory fees for tax years 2018 through 2025. Previously, these fees were deductible as a miscellaneous itemized deduction subject to the 2% floor. This means you're paying advisor fees with after-tax dollars, making the actual cost higher than the nominal fee amount.

How do I know if my financial advisor fees are reasonable?

Compare what you're paying to industry benchmarks for similar services. Calculate the actual dollar amount, not just the percentage. Ask what specific services you're receiving for that fee. Consider whether the fee has grown significantly as your portfolio appreciated, and whether that increase corresponds to additional service or complexity. If you're paying more than $15,000 annually, it's worth exploring whether you could receive comparable service through alternative fee structures.

What's the difference between fee-only and fee-based advisors?

Fee-only advisors are compensated exclusively through fees paid directly by clients (AUM, flat fee, or hourly). They don't receive commissions from selling products. Fee-based advisors can charge fees AND receive commissions from product sales, creating potential conflicts of interest. When evaluating advisors, look for fee-only fiduciaries who are legally required to act in your best interest.

The Bottom Line

Here's what I believe after years in this industry.

Financial advice has genuine value. A good advisor helps you avoid costly mistakes, optimize your strategy, and make better decisions. That's worth paying for.

But the fee structure should match the service provided and the value delivered for your specific situation. What made sense when you had a $300,000 portfolio may or may not make sense now that you have $1.5 million.

If you have substantial assets and you're paying 1% or more in AUM fees, consider running the numbers on what that actually costs you in dollars, not percentages. Understand what you're paying for. Compare that to what alternative arrangements might look like for comparable service.

You might conclude your current arrangement is fair and you're happy with it. That's a perfectly valid outcome. Or you might discover there are alternatives worth exploring.

Either way, it's your money. You should know exactly what you're paying for it.

Important Disclosure This article provides general information about financial advisor fee structures and is not personal financial advice. Nothing in this article should be considered a recommendation to change advisors or fee arrangements, and reading this content does not create an advisor-client relationship. The decision to work with a financial advisor and which fee structure to choose depends on your unique financial situation, complexity of needs, and personal preferences. All fee examples and savings calculations shown in this article are illustrative only and intended for comparison purposes. Actual fees vary widely based on services provided, individual circumstances, portfolio performance, and many other factors. Past fee arrangements do not guarantee future costs. This content is for educational purposes only. The author is a fee-only fiduciary financial advisor operating on a flat-fee basis serving clients in the Orlando, Florida area. Before making decisions about your financial advisor relationship or fee structure, consider consulting with the advisor about your specific needs and circumstances, and consider seeking a second opinion if desired.